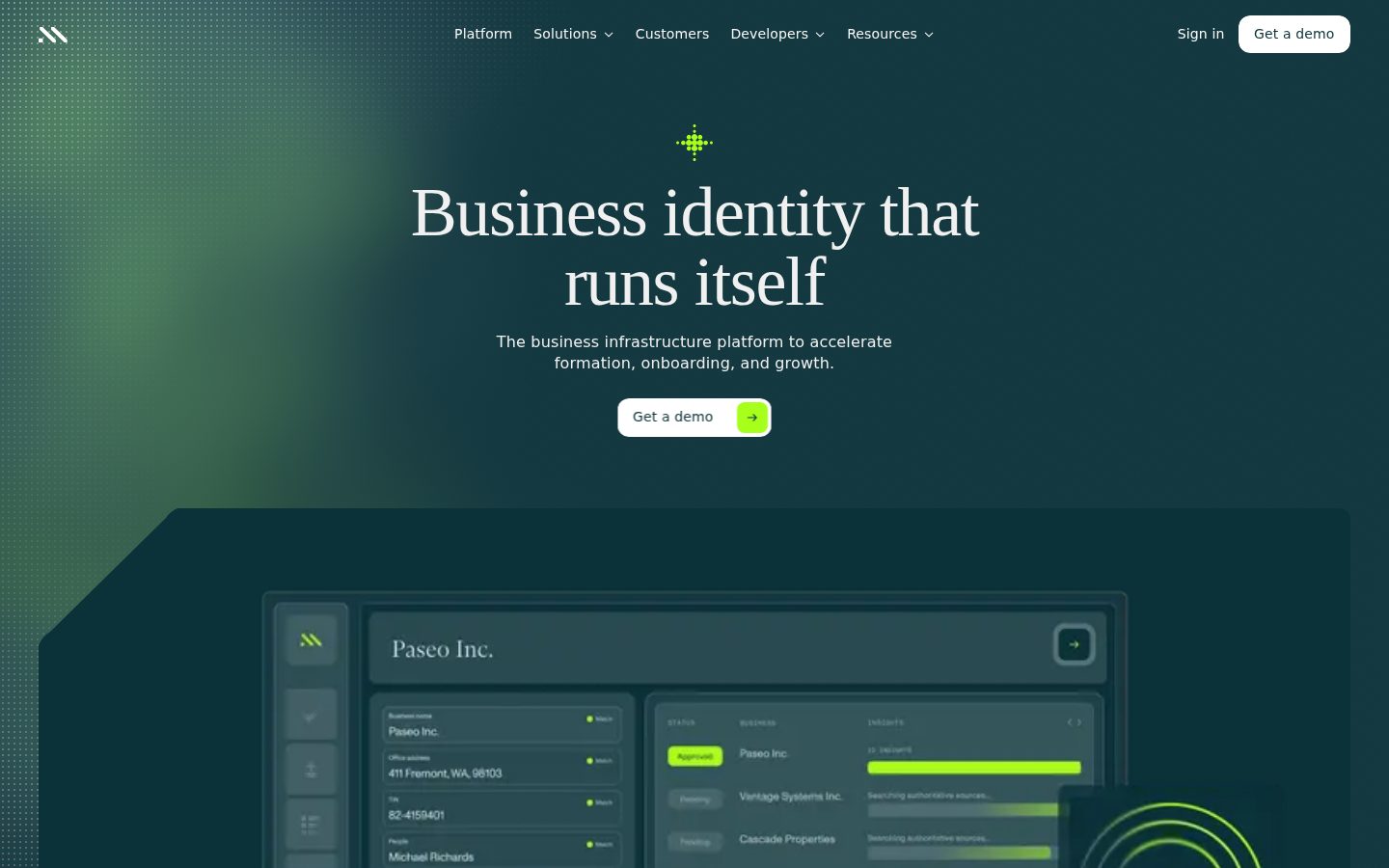

In practice, Middesk integrates into a financial platform's onboarding flow and handles business identity verification end-to-end. When an application comes in, Middesk pulls entity data from government registries and other authoritative sources, runs it through fraud and risk models, and either resolves the application automatically or flags it for human review. The goal is that analysts only see edge cases — not every submission.

The platform covers four distinct functional areas: KYB (Know Your Business) verification, fraud prevention, underwriting support, and business registration. The fraud module uses purpose-built machine learning models alongside AI agents that map ownership networks and digital footprints to detect synthetic identities. The underwriting component provides entity data and lifecycle intelligence to support credit modeling, including UCC filing management. The registration product handles state and federal agency filings on behalf of businesses embedded within the platform.

Middesk is built for regulated industries — specifically banks, fintechs, lenders, and financial platforms where compliance and auditability are requirements. The platform is SOC 2 Type II certified and maintains audit-friendly records explaining why individual businesses were approved or declined. Competitors in the KYB and business verification space include Persona, Socure, LexisNexis Risk Solutions, and Enigma. Pricing is not publicly listed; prospective customers must request a demo to obtain pricing details.

Middesk is a web-based platform and offers API integration for embedding verification and registration capabilities directly into customer-facing products. The company reports verifying 7 million businesses annually and processing over $100 billion in revenue flows through its infrastructure.