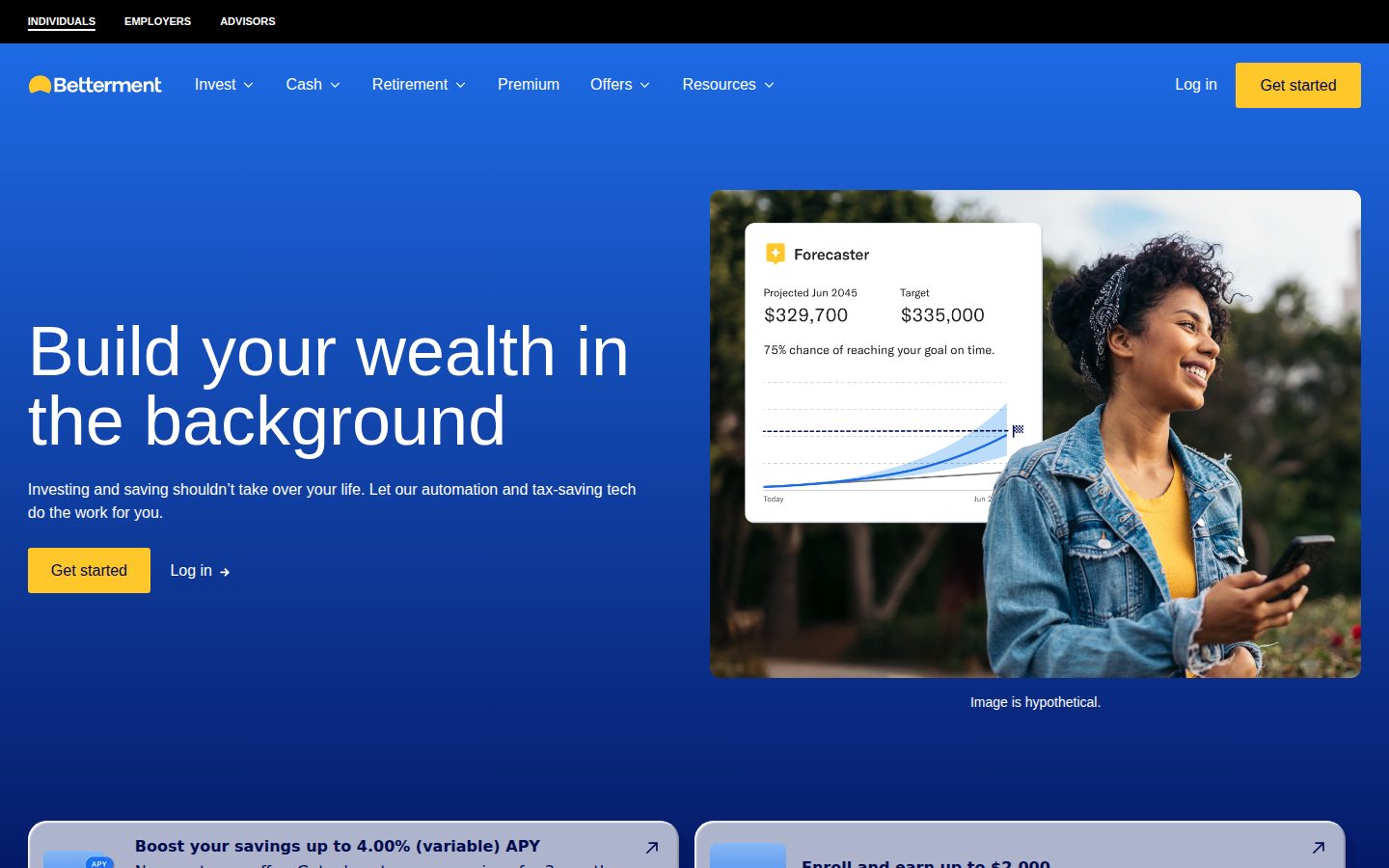

Users sign up, answer questions about their financial goals and risk tolerance, and are placed into diversified ETF-based portfolios. From there, Betterment handles ongoing portfolio management automatically—rebalancing allocations, reinvesting dividends, and applying tax-loss harvesting without requiring manual input. Users can set multiple goal-based buckets (retirement, emergency fund, large purchase) and track progress across all of them in a single dashboard.

Beyond the core automated investing account, Betterment offers a high-yield cash account (Cash Reserve) with FDIC insurance up to $8 million for joint accounts through its network of program banks—16x the standard FDIC limit at most firms. It also provides traditional, Roth, and SEP IRAs with automated tax coordination across account types, and a self-directed investing option where users can trade individual stocks and ETFs with no commission or management fees and see tax impact estimates before executing a sale. A Premium plan tier at an additional 0.40% annual fee unlocks unlimited access to licensed human financial advisors, with a $100,000 minimum balance requirement.

Betterment targets individual investors who want a low-effort, automated approach to building wealth—particularly those who do not want to actively manage portfolios. The platform operates as a registered investment adviser and acts as a fiduciary. Management fees for automated investing accounts are percentage-based; the self-directed investing account carries no management fee. Competitors in the robo-adviser category include Wealthfront, SoFi Invest, and Schwab Intelligent Portfolios. Vanguard Digital Advisor and Fidelity Go are comparable offerings from traditional brokerages.

Betterment is accessible via web browser and mobile apps on iOS and Android. Customer support is available five days per week; human advisor access requires the Premium plan or an additional per-session fee. Checking accounts are offered through a partnership with nbkc bank, Member FDIC.