Users open a Cash Account, Automated Investing Account, or Stock Investing Account through Wealthfront's web or mobile app. The Automated Investing Account builds a personalized portfolio of index funds based on a risk score (0.5–10), then manages it continuously — rebalancing, reinvesting dividends, and applying tax-loss harvesting automatically. The Stock Investing Account allows self-directed buying of individual stocks and ETFs with zero commissions and a $1 minimum.

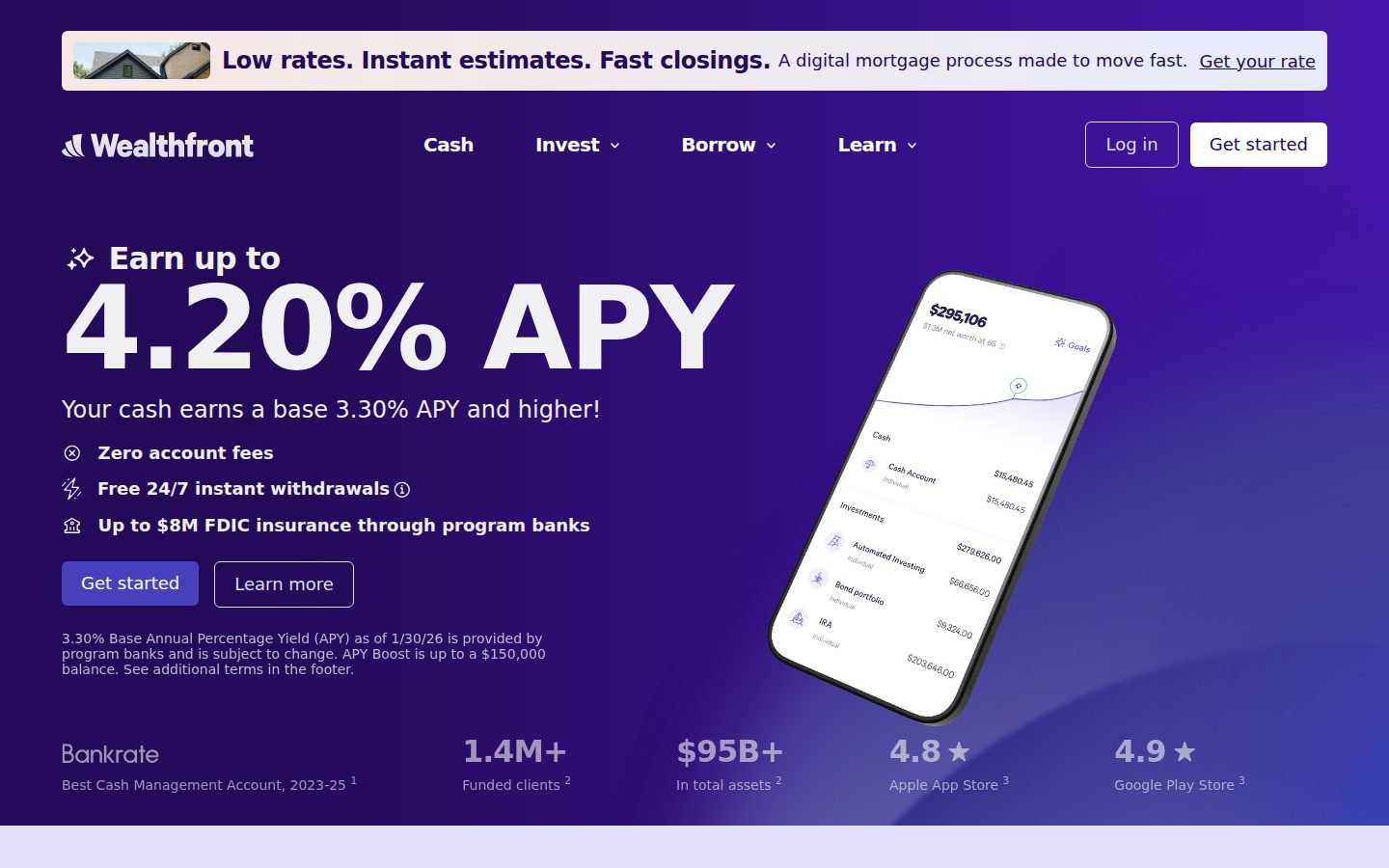

Wealthfront highlights several specific capabilities on its platform: Tax-Loss Harvesting, S&P 500 Direct Indexing, an Automated Bond Ladder, and a 529 Education Savings Plan. The Cash Account supports up to $8M in FDIC insurance through a network of program banks, and APY can be raised above the 3.30% base rate through a new-client boost (0.65% for 3 months on up to $150,000) or a permanent 0.25% increase tied to a $1,000/month direct deposit plus an active investing account. As of February 2026, the platform reports a 9.83% average annual return since inception for its Classic Automated Investing Account at a composite risk score of 9.

Wealthfront targets individual investors who want to automate savings and investing without ongoing advisor interaction. The platform charges zero account fees on its Cash Account and zero commissions on stock trades; the Automated Investing Account carries a 0.25% annual advisory fee (not stated on the homepage but a widely published figure). Competitors in the robo-advisor space include Betterment, Fidelity Go, and Schwab Intelligent Portfolios; Wealthfront has received external recognition specifically for direct indexing and tax-loss harvesting relative to Fidelity, Schwab, and Vanguard.

Wealthfront is accessible via web browser and mobile apps on iOS (4.8 App Store rating) and Android (4.9 Google Play rating). The platform also trades publicly on the NASDAQ under the ticker WLTH.