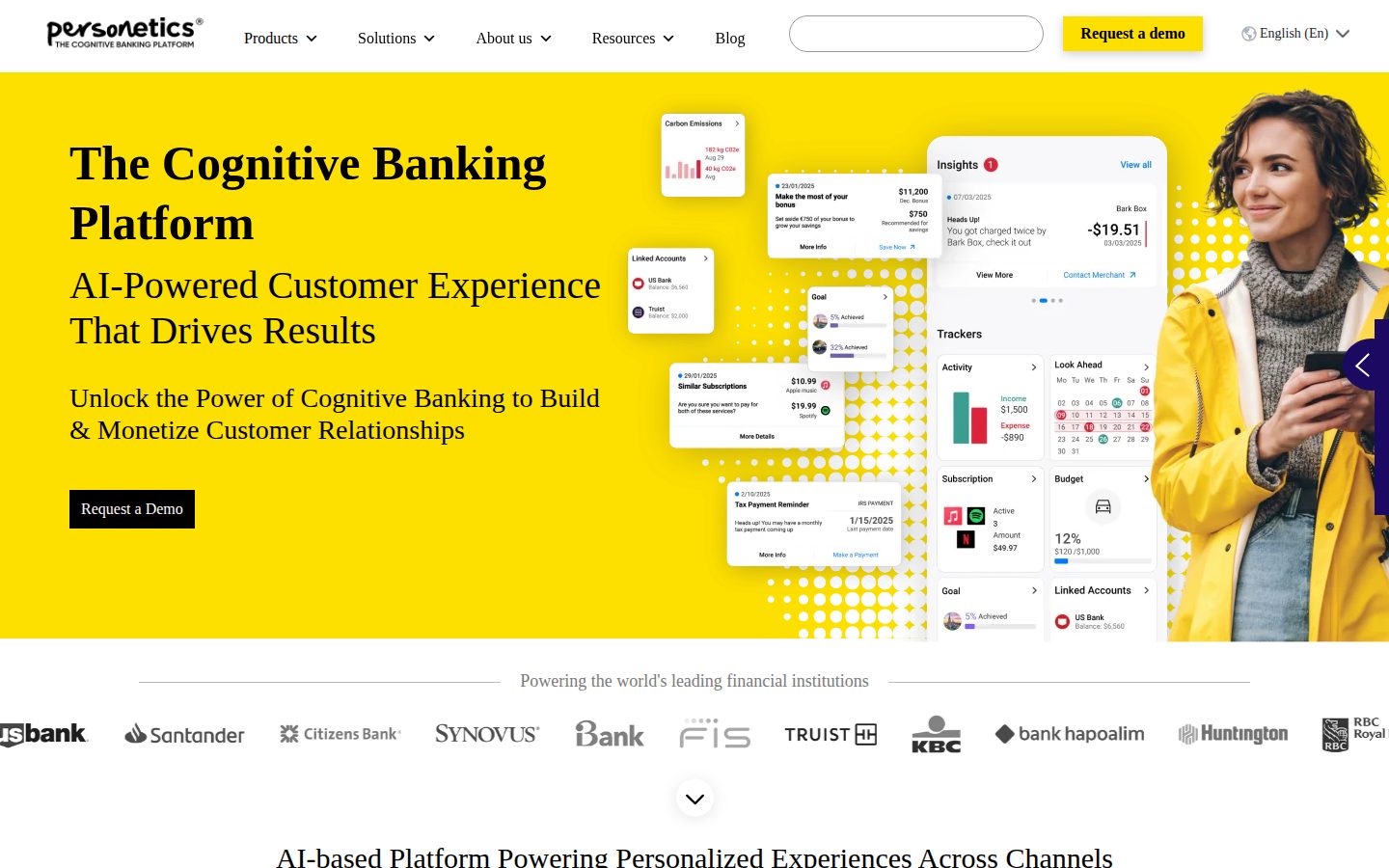

Banks integrate Personetics into their mobile and online banking platforms, where it processes customer transaction histories to surface contextual alerts, spending summaries, budget tracking, and automated savings triggers. End customers interact with the output through their bank's existing app or web interface, seeing personalized financial tips, cash flow forecasts, and goal-based savings journeys without leaving the banking experience they already use.

The platform offers several distinct capability areas: personal financial management (PFM) with data cleansing, enrichment, and categorization; hyper-personalized insights and advice designed to increase product engagement and cross-sell; goal-based savings automation including auto-save features; and a dedicated small business suite covering cash flow forecasting for both customers and relationship bankers. Personetics also provides what it calls Self-Driving Finance capabilities, which trigger automated financial actions on behalf of customers based on detected patterns. The system is delivered as a SaaS model, allowing banks to continuously receive new insight content without custom development.

Personetics is built exclusively for financial institutions — retail banks, credit unions, and digital banks — rather than end consumers directly. Pricing is not publicly listed; prospective customers are directed to request a demo, indicating an enterprise contract model. The company operates in a category that includes competitors such as MX Technologies, Bud Financial, Meniga, and Backbase, all of which offer varying degrees of transaction data enrichment and personalized banking experiences.

The platform supports deployment across web and mobile banking channels and is available in multiple languages including English, Italian, Portuguese, Spanish, Japanese, French, and German. Personetics has published integrations with Microsoft Azure infrastructure and Q2 Innovation Studio, and clients include Scotiabank, U.S. Bank, Huntington Bank, Santander, UOB, Erste Group, KBC, BMO, Ally, and Akbank, among others. The company reports serving 150 million monthly users across 30 global markets.